Estate Planning for Real Estate Investors and Landlords: A Guide

April 30, 2026

As a California real estate investor, you’ve spent years acquiring rental homes and commercial buildings. But without a plan, you’re leaving your heirs a nightmare: a tangled web of public probate filings, shocking property tax reassessments, and potential family disputes. A solid strategy for estate planning for real-estate investors and landlords is the only way to bypass this mess. It protects the portfolio you worked so hard to build, ensuring your estate planning for rental property and commercial real estate assets transfer smoothly and continue generating income for the next generation.

Schedule a strategy session with Lawvex to start building an estate plan that protects your real estate investments and your family’s future.

This guide covers the specific strategies California real estate investors need, from choosing the right trust structure to navigating Proposition 19 property tax rules. Whether you own two rental houses or twenty, the principles below will help you transfer wealth without unnecessary taxes, delays, or conflict among your beneficiaries.

Why Your Real Estate Portfolio Needs a Custom Estate Plan

A standard will or basic trust might work for someone with a primary residence and a savings account. Real estate investors face a different set of challenges that demand specialized planning.

First, every California property you own at death must go through probate unless it is held in a trust or has another transfer mechanism in place. Probate in California is public, slow (often 12 to 18 months), and expensive. Statutory attorney and executor fees are based on the gross value of the estate, not equity. A rental property worth $800,000 with a $500,000 mortgage still counts as $800,000 for fee calculations. Multiply that across several properties, and probate costs can reach tens of thousands of dollars.

Second, rental properties need active management. Tenants pay rent, maintenance requests come in, and insurance premiums are due, all of which require someone with legal authority to act. Without an estate plan that names a successor trustee or agent, your properties can sit in limbo while courts sort things out. Vacancies pile up. Bills go unpaid. Value erodes.

Third, California’s property tax rules create unique planning considerations. Under Proposition 13 and its successor Proposition 19, the tax basis of inherited property can change dramatically depending on how the transfer is structured. Getting this wrong can cost your heirs thousands of dollars per year, per property.

Key Financial Metrics Real Estate Investors Use

Before we get into the legal structures that protect your properties, it’s helpful to understand how investors evaluate them in the first place. Building a successful real estate portfolio isn’t about luck; it’s about making smart, data-driven decisions. Many seasoned investors rely on simple rules of thumb to quickly analyze a potential deal’s profitability. These metrics help them filter out underperforming properties and focus on assets that will generate consistent cash flow and long-term growth. Understanding these calculations gives you insight into the value you’re building and why it’s so critical to protect it for the future.

The 2% Rule: A Quick Cash Flow Check

One of the most common quick tests is the 2% rule. As the real estate resource Rentana explains, “The rule says that the monthly rent should be equal to or more than 2% of the property’s purchase price.” For example, if you buy a rental home for $400,000, this rule suggests it should generate at least $8,000 in monthly rent to be a strong investment. While this metric is a great starting point for assessing cash flow, it can be challenging to meet in high-cost areas like those in California. It’s a useful benchmark for comparison, but don’t be discouraged if your properties fall short; other factors like appreciation and tax benefits also contribute to your overall return.

The 7% Rule: An Annual Return Guideline

Another helpful guideline is the 7% rule, which looks at returns from an annual perspective. This rule “suggests that the total rent a property brings in each year should be at least 7% of what the property cost to buy.” Using this logic, a $600,000 property should bring in at least $42,000 in gross annual rent ($3,500 per month). This metric provides a broader view of a property’s performance over the year. Like the 2% rule, it’s a simplified tool to help you evaluate potential investments quickly, not a strict requirement for success.

Why a Will Isn’t Enough for Real Estate Investors

Many people assume that creating a will is all they need to do to pass their assets to their loved ones. While a will is a fundamental part of any estate plan, it falls short for anyone who owns real estate, especially a portfolio of investment properties. Relying solely on a will guarantees your estate will go through the California probate court system. This public process is notoriously slow and expensive, often freezing your assets for a year or more while your heirs wait for a judge’s approval to manage or sell the properties. This delay can lead to lost rental income, missed opportunities, and declining property values.

Furthermore, a will offers no protection against the administrative headaches that come with an active real estate portfolio. As one law firm notes, “You’d have to update your will every time you buy or sell a property.” This is impractical for an active investor. A far better solution is to place your properties into a revocable living trust. A trust allows you to administer your portfolio seamlessly during your lifetime and designates a successor trustee to take over immediately upon your death or incapacity, completely bypassing probate. This ensures your properties continue to be managed, rents are collected, and your family is provided for without any court intervention or costly delays.

Start Here: The Revocable Living Trust

A revocable living trust is the cornerstone of real estate investor estate planning in California. When you transfer your properties into a revocable trust, you maintain full control during your lifetime. You can buy, sell, refinance, and manage every property exactly as before. The trust simply replaces you as the legal owner on the deed.

The key benefits for investors include:

- Probate avoidance: Properties held in a trust pass directly to your beneficiaries without court involvement, saving months of delay and thousands in fees.

- Privacy: Trust transfers do not become public record the way probate proceedings do, keeping your portfolio details confidential.

- Incapacity protection: If you become unable to manage your properties, your successor trustee steps in immediately. No court petition required. Rents keep getting collected, mortgages keep getting paid, and tenants stay managed.

- Continuity of operations: Your successor trustee can handle property management, make repair decisions, and even sell properties if needed, all according to the instructions you set in the trust document.

Every rental property, vacation home, and vacant lot you own should be deeded into your trust. Forgetting to transfer even one property means that asset goes through probate, which defeats much of the purpose of the trust. A pour-over will can catch missed assets, but the goal is to avoid that fallback entirely.

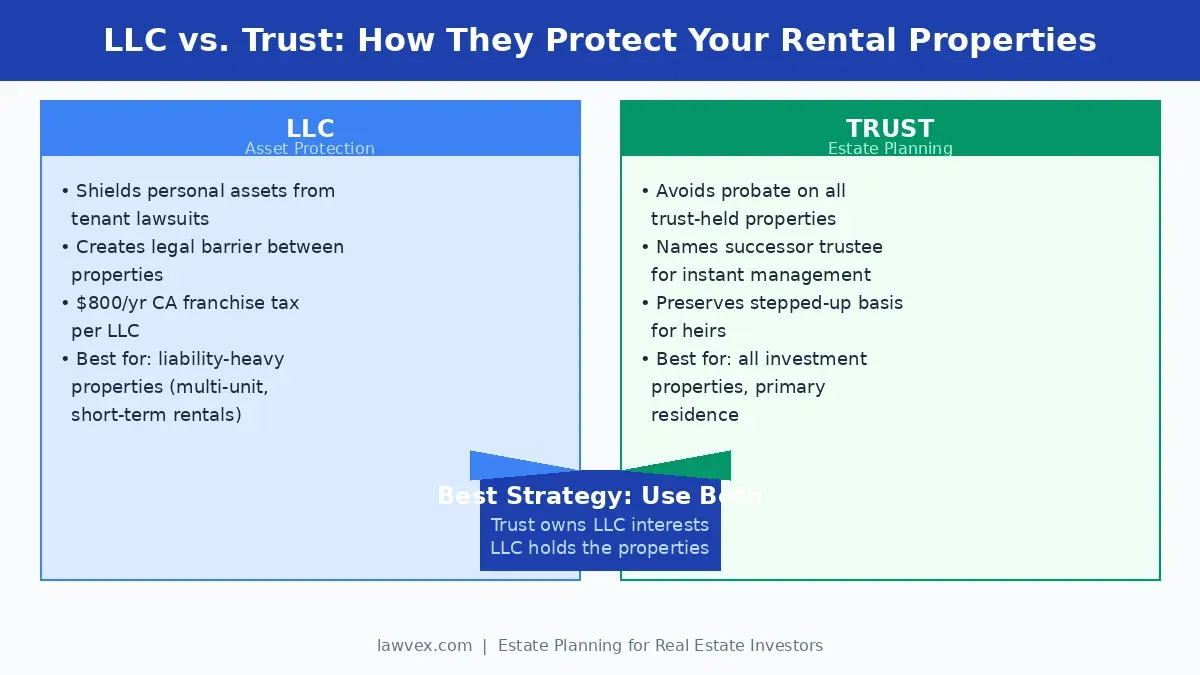

LLC or Trust: What’s Best for Your Rental Properties?

One of the most common questions real estate investors ask is whether they should hold rental properties in an LLC or a trust. The answer for most California investors is both, because each serves a different purpose.

LLC vs. Trust for rental properties: An LLC shields your personal assets from lawsuits related to a specific rental property, while a trust ensures the property passes to your heirs without probate. Most investors benefit from using both structures together.

An LLC provides liability protection. If a tenant slips on the stairs of your fourplex and sues, the lawsuit targets the LLC that owns that property, not your personal assets or other properties in separate LLCs. California is one of the more expensive states for LLC formation and maintenance, with an $800 minimum annual franchise tax per LLC, plus the standard filing fees. That cost is worth considering when you decide how to allocate your properties.

A trust provides estate planning benefits. It keeps your properties out of probate, allows for incapacity management, and lets you control how and when your beneficiaries receive their inheritance.

The recommended structure for many investors works like this:

- Create a revocable living trust as the core estate planning vehicle.

- Form one or more LLCs to hold your rental properties (grouping properties by risk level or geographic area).

- Make the trust the member of each LLC, so you get both liability protection and probate avoidance.

- When you pass away, the trust distributes the LLC membership interests to your beneficiaries according to your instructions.

This layered approach lets you separate lawsuit risk across LLCs while keeping everything organized under one trust for estate planning purposes.

fee if revenue exceeds $250,000. For investors with just one or two lower-value rentals, the cost of maintaining separate LLCs may not be justified. For portfolios with higher liability exposure (multi-unit buildings, short-term rentals, or properties in high-traffic areas), the protection is usually worth the expense.

Not sure which structure makes sense for your portfolio? Contact Lawvex for a personalized assessment of your real estate holdings.

Using a Series LLC for Added Protection

If your portfolio includes several properties, putting them all into a single LLC can feel like putting all your eggs in one basket. A lawsuit involving one property could potentially expose the assets of the entire LLC. This is where a Series LLC offers a more sophisticated layer of protection. Think of it as a parent company with several independent subsidiaries, or “series,” underneath it. Each series can own a single property, have its own assets, and be insulated from the liabilities of the other series. This structure, a key component of advanced business planning for investors, effectively firewalls each of your investments from the risks associated with the others.

The Role of Land Trusts for Privacy

For many real estate investors, privacy is a top priority. A land trust is a simple yet powerful tool designed specifically for this purpose. When you use a land trust, the trust itself holds the legal title to your property, and your name as the owner does not appear on public records. You remain the beneficiary, retaining full control and all the benefits of ownership. This anonymity can be a significant deterrent to frivolous lawsuits and unwanted solicitations. Furthermore, when combined with your revocable living trust, it simplifies the transfer of property to your heirs, keeping the details of your portfolio confidential since trust transfers are not part of the public probate process.

How a Stepped-Up Basis Saves Your Heirs from Capital Gains Tax

One of the most valuable tax benefits available to real estate investors is the stepped-up basis at death. Understanding how it works is essential for structuring your estate plan correctly.

When you buy a rental property for $300,000 and it appreciates to $900,000 by the time you pass away, your heirs receive it with a new tax basis of $900,000, the fair market value at the date of your death. If they sell it for $920,000, they owe capital gains tax on only $20,000, not the $600,000 in appreciation that occurred during your lifetime.

This is a significant advantage for real estate investors who have held properties for decades in appreciating California markets. The stepped-up basis effectively erases years of depreciation recapture and capital gains in a single transfer.

However, the stepped-up basis only applies to assets included in the decedent’s taxable estate. Certain irrevocable trust structures and gifting strategies can inadvertently eliminate this benefit. For example, if you gift a rental property to your children during your lifetime, they receive your original cost basis (the carryover basis), not the stepped-up value. On a property with $600,000 in appreciation, that mistake could cost them over $100,000 in capital gains tax.

The takeaway: for most real estate investors, holding appreciated properties in a revocable living trust until death is the most tax-efficient transfer strategy. Lawvex estate planning attorneys help investors structure these transfers to maximize the stepped-up basis benefit across their entire portfolio.

What Real Estate Investors Should Know About Prop 19

California’s Proposition 19, which took effect in February 2021, fundamentally changed the property tax rules for inherited real estate. Every investor with California property needs to understand how it affects their estate plan.

The Old Rules: Before Prop 19

Under the old rules (Proposition 58), parents could transfer their primary residence and up to $1 million in assessed value of other properties to their children without triggering a property tax reassessment. This was a massive benefit for investors. A rental property purchased in 1990 for $150,000, now worth $800,000, could pass to a child with the original low property tax basis intact.

The New Rules: After Prop 19

Proposition 19 eliminated the parent-child exclusion for all investment and rental properties. Now, when your children inherit a rental property, it will be reassessed at current fair market value, which can increase the annual property tax bill by thousands of dollars.

The only exclusion that remains is for a primary residence, and even that is limited. A child must use the inherited home as their own primary residence and file a homeowner’s exemption within one year of the transfer. If the home’s fair market value exceeds the original assessed value by more than $1 million, only the first $1 million in value is excluded from reassessment.

How This Impacts Your Investment Strategy

If you own multiple rental properties with low Proposition 13 tax bases, your heirs will face significantly higher property taxes after inheriting them. Lawvex attorneys work with California real estate investors to navigate these complex Proposition 19 rules and minimize the tax impact on inherited properties. This changes the calculus on several estate planning decisions:

- Hold vs. sell analysis: It may make more sense to sell certain properties before death, pay the capital gains tax, and leave liquid assets to heirs rather than properties with soon-to-be-inflated tax bills.

- Entity structuring: Transferring properties through LLCs or partnerships can sometimes be structured to minimize reassessment triggers, though California rules are strict about this.

- Cash reserves: Your estate plan should account for the increased property tax burden your heirs will face and ensure sufficient liquid assets are available to cover costs during the transition period.

How 1031 Exchanges Fit Into Your Estate Plan

Many California real estate investors use 1031 exchanges to defer capital gains taxes when selling one investment property and buying another. These exchanges are powerful wealth-building tools, but they create specific estate planning considerations.

When you do a 1031 exchange, the deferred gain carries forward to the replacement property. You have not avoided the tax; you have postponed it. However, if you hold the replacement property until death, your heirs receive the stepped-up basis, effectively eliminating the deferred gain permanently.

This creates a compelling long-term strategy:

- Use 1031 exchanges throughout your investing career to defer gains and grow your portfolio.

- Hold the final set of replacement properties in your revocable trust.

- At death, the stepped-up basis wipes out all accumulated deferred gains.

The result is a lifetime of tax-deferred growth followed by a tax-free transfer to the next generation (at least with respect to capital gains). This is one of the most powerful wealth-building strategies available to real estate investors, and it only works with proper estate planning in place.

One caution: if you are in the middle of a 1031 exchange and die before it is completed, the exchange can fail. Your estate plan should include specific provisions for completing pending exchanges. Your successor trustee needs the authority and the knowledge to identify replacement properties and close within the IRS deadlines.

A Guide to Managing Multiple Properties in a Trust

Investors with large portfolios need their trust to address operational realities that go beyond basic estate planning. Your trust document should cover:

Assigning a Property Manager

Your successor trustee needs clear authority to manage rental properties. This includes collecting rents, paying mortgages and property taxes, hiring property managers, approving repairs, screening tenants, and executing leases. Without explicit authority in the trust document, your successor trustee may face challenges taking these routine management actions.

Setting Clear Decision-Making Rules

Should your successor trustee sell properties or hold them for rental income? Can they refinance to pull out equity? Should they distribute rental income to beneficiaries or reinvest it? These are policy decisions you should make in your trust, not leave to guesswork during a stressful transition period.

Leaving Instructions for Each Property

If you want certain properties to go to specific beneficiaries, spell that out clearly. For example, you might want your son to receive the apartment building he has been managing, while your daughter gets the commercial property near her business. Specific distributions reduce family conflict and ensure each heir receives property that matches their interests and abilities.

Planning for Maintenance and Repairs

Your trust should designate funds for property maintenance and unexpected repairs. A new roof on a commercial building can cost $50,000 or more. Without reserves set aside, your successor trustee may be forced to sell a property at a bad time just to cover necessary repairs.

, such as:

- Whether the trustee should retain or sell specific properties

- How rental income should be distributed among beneficiaries

- Authority to hire property managers, make capital improvements, and refinance

- Guidelines for handling tenant disputes and vacancy decisions

- A process for beneficiaries who want to buy out other beneficiaries’ interests in a property

Clear instructions prevent family disagreements and give your successor trustee the confidence to act decisively when managing your portfolio.

Solving the “Property-Rich, Cash-Poor” Problem

Many successful real estate investors in areas like Clovis and Madera are “property-rich but cash-poor.” Your net worth looks great on paper, but most of it is tied up in equity, leaving little liquid cash. This becomes a major issue when you pass away. Your estate will need cash to pay for administration costs, final taxes, and ongoing property expenses. With Proposition 19 triggering property tax reassessments, your heirs will face higher annual bills right away. Without a source of funds, your successor trustee might be forced to sell a prized rental property quickly, possibly at a discount, just to cover these costs. A well-designed estate plan anticipates this by creating a liquidity fund, often through a life insurance policy owned by the trust, to ensure your family has the cash it needs to keep your portfolio intact.

Giving Beneficiaries Access: The “5 by 5” Power

As a property owner, you want to protect your assets for your beneficiaries, but you also don’t want to tie their hands completely. The “5 by 5 power” is a feature you can include in a trust to strike this balance. It gives a beneficiary the right to withdraw a certain amount from the trust each year without needing the trustee’s approval. The amount is the greater of $5,000 or 5% of the trust’s total value. This gives your heirs a predictable source of funds for personal expenses, a down payment, or an investment opportunity, all while the rest of the trust assets remain protected. Best of all, the money they withdraw under this rule is typically not counted as taxable income. It’s a smart way to provide flexibility and autonomy within the secure framework of a trust administration.

Is a Transfer on Death (TOD) Deed Right for You?

California allows property owners to use a Transfer on Death Deed (TODD) to pass real estate to a named beneficiary without probate. While this sounds appealing, it has significant limitations for real estate investors.

A TODD only works for a single property and a single beneficiary (or a small number of beneficiaries). It cannot include conditions, management instructions, or the kind of detailed planning that a trust provides. If you own multiple properties, you would need a separate TODD for each one, and none of them would include provisions for ongoing management or distribution of rental income.

TODDs also expire after 60 days if the owner does not die within that period (though they can be re-recorded). For most real estate investors, a revocable living trust remains the better option. However, a TODD can serve as a useful backup for a property that was accidentally left out of the trust.

Married? How Community Property Affects Your Portfolio

California is a community property state, which creates both opportunities and complications for married real estate investors.

Property acquired during marriage with community funds is generally community property, meaning each spouse owns an equal half. When one spouse dies, the surviving spouse’s half and the deceased spouse’s half both receive a stepped-up basis. This double step-up is a significant tax advantage unique to community property states.

However, investors who acquired properties before marriage, received them as gifts, or purchased them with separate funds may hold a mix of community and separate property. Commingling of funds (using rental income from a separate property to pay the mortgage on a community property, for example) can blur the lines and create disputes.

Your estate plan should clearly identify each property’s character (community or separate) and include provisions for managing both types within the trust.

Planning for Your Potential Incapacity

An estate plan isn’t just about what happens after you die; it’s also about protecting your assets if you become unable to manage them yourself. For a real estate investor, incapacity—whether from an accident, illness, or cognitive decline—can be financially devastating. Your properties require constant management. If you’re suddenly unable to act, who has the legal authority to collect rent, pay the mortgage, or handle an emergency repair? Without a plan, the answer is no one. Your properties can sit in limbo while your family petitions the court for control. During that time, vacancies can pile up, bills go unpaid, and the value of your portfolio can quickly erode.

This is where your revocable living trust proves its immense value. If you become incapacitated, your designated successor trustee can step in immediately to manage the properties held within your trust. Because the trust already grants them this authority, there is no need for court intervention. This seamless transition means rents keep getting collected, mortgages get paid, and tenants stay managed. Your portfolio continues to operate without interruption, preserving your income stream and protecting the assets you’ve worked so hard to build. It provides peace of mind that your investments are secure, no matter what life throws your way.

The Importance of a Durable Power of Attorney

While a successor trustee manages assets held inside your trust, a Durable Power of Attorney for finances covers everything else. This essential legal document allows you to appoint a trusted person—your “agent”—to manage financial matters outside of your trust if you become incapacitated. This can include accessing personal bank accounts to pay your bills, filing tax returns, or dealing with retirement accounts. A comprehensive estate plan ensures someone has the authority to handle all your financial affairs. Without a Durable Power of Attorney, your family would be forced into a court process called a conservatorship, which is public, expensive, and time-consuming, just to gain the ability to manage your finances.

Tax Strategies for High-Value Real Estate Portfolios

The current federal estate tax exemption is approximately $13.99 million per individual ($27.98 million for married couples) as of 2025. California does not impose a separate state estate tax. Most real estate investors will fall below these thresholds.

However, if your combined real estate portfolio, retirement accounts, life insurance, and other assets approach or exceed the exemption amount, additional planning tools become relevant:

- Irrevocable trusts: Moving assets into an irrevocable trust removes them from your taxable estate, though you give up control. This makes more sense for investors who have older properties they do not actively manage.

- Family Limited Partnerships (FLPs): Holding rental properties in an FLP allows you to gift limited partnership interests to children at a discounted value, reducing the size of your taxable estate over time.

- Charitable Remainder Trusts: If you have a highly appreciated property and charitable intentions, a CRT can provide a lifetime income stream, an immediate tax deduction, and estate tax reduction.

The estate tax exemption is scheduled to change after 2025, potentially dropping to around $7 million per person. Investors with portfolios in the $5 million to $15 million range should pay close attention to these changes and plan accordingly.

Want to know how upcoming estate tax changes affect your real estate portfolio? Contact Lawvex today to discuss your options before the exemption potentially decreases.

Strategic Gifting to Reduce Your Taxable Estate

For investors with estates large enough to face potential estate taxes, gifting properties during your lifetime can seem like a smart move. By giving a rental property to your children now, you remove its value—and all future appreciation—from your taxable estate. The IRS allows you to give a certain amount to anyone each year without filing a gift tax return, and there’s a much larger lifetime exemption for gifts that exceed the annual limit. While this strategy can reduce your estate tax bill, it comes with a major trade-off for your heirs: the loss of the stepped-up basis. They will inherit the property with your original cost basis, potentially facing a massive capital gains tax bill if they ever sell.

Advanced Tool: The Qualified Personal Residence Trust (QPRT)

A Qualified Personal Residence Trust, or QPRT, is a specialized tool for transferring a primary residence or vacation home out of your taxable estate at a reduced gift tax value. Here’s how it works: you transfer the home into an irrevocable trust but retain the right to live in it for a specific number of years. If you outlive that term, the house officially passes to your beneficiaries, free of estate tax. The initial gift value is calculated at a discount because of your retained right to live there. This is an advanced strategy with specific risks—if you don’t outlive the term, the property reverts to your estate. It’s a powerful tool, but one that requires careful consideration with an estate planning attorney.

Understanding the Generation-Skipping Transfer Tax (GSTT)

If your plan involves leaving property directly to your grandchildren, you need to be aware of the Generation-Skipping Transfer Tax (GSTT). This is a separate federal tax levied on transfers to beneficiaries who are more than one generation younger than you, known as “skip persons.” The tax is steep, applied at the highest estate tax rate on top of any applicable estate taxes. Like the federal estate tax, there is a lifetime GSTT exemption. For most families, their total estate will fall under this exemption amount. However, for high-net-worth investors, structuring a trust to properly allocate the GSTT exemption is crucial for protecting the wealth you intend to pass down to future generations.

Factoring in Property Transfer Taxes

As we covered earlier, Proposition 19 has completely changed the landscape for inherited rental properties in California. The old parent-child exclusion that protected investment properties from reassessment is gone. Now, when your children in Clovis or Madera inherit your rental portfolio, every single property will be reassessed at its current market value. This can cause the annual property tax bill to skyrocket, turning a cash-flowing asset into a financial burden. A successful estate plan for a California real estate investor must now include a strategy for managing this inevitable tax increase, whether through setting aside cash reserves or structuring the sale of certain properties.

Avoiding Pitfalls: The Retained Interest Rules

The IRS is wise to attempts to give away property while still keeping all the benefits. The “retained interest” rules are designed to prevent this. If you gift a rental property to your son but continue to collect the rent and use it for your personal expenses, the IRS will likely determine that you retained an economic interest. In that case, the property will be pulled back into your estate for tax purposes, defeating the purpose of the gift. This is why DIY transfers are so risky. A properly structured gift or trust ensures the transfer is complete and legally binding, avoiding pitfalls that could undo your entire trust administration strategy.

Frequently Asked Questions

Can I still get a mortgage on a property held in a trust?

Yes. Most lenders will work with properties held in a revocable living trust. You may need to temporarily transfer the property out of the trust to close the loan, then transfer it back. Some lenders will lend directly to the trust. Either way, the process is routine and should not prevent you from refinancing or obtaining new loans on trust-held properties.

Do I need a separate trust for each property?

No. A single revocable living trust can hold all of your properties. However, you may want separate LLCs for different properties to isolate liability risk. The trust can be the member of multiple LLCs, keeping everything organized under one estate planning umbrella.

What happens to my properties if I become incapacitated without a trust?

Without a trust or durable power of attorney, your family would need to petition the court for a conservatorship to manage your properties. This is expensive, time-consuming, and public. A trust with a named successor trustee avoids this entirely.

How does Proposition 19 affect my rental properties?

When your heirs inherit rental or investment properties, those properties will be reassessed at current fair market value under Proposition 19. The parent-child exclusion that previously protected these transfers was eliminated for non-primary-residence properties. Your estate plan should account for the increased property tax burden your heirs will face.

Should I gift rental properties to my children now or leave them in my estate?

In most cases, leaving appreciated rental properties in your estate is more tax-efficient than gifting them during your lifetime. Properties you hold until death receive a stepped-up basis, eliminating capital gains tax for your heirs. Gifted properties carry your original cost basis, which can create a substantial tax bill when your children eventually sell.

Putting Your Real Estate Estate Plan into Action

Real estate investor estate planning requires more than a standard trust or will. Your plan needs to address LLC structuring, stepped-up basis optimization, Proposition 19 property tax impacts, 1031 exchange considerations, and detailed property management instructions for your successor trustee.

The attorneys at Lawvex work exclusively with California clients on estate planning, trust administration, and probate matters. We understand the specific challenges real estate investors face and build estate plans that protect portfolios of every size.

Schedule a strategy session with Lawvex to start building an estate plan tailored to your real estate investment portfolio. We will review your current holdings, identify tax-saving opportunities, and create a plan that protects your properties and your family’s financial future.

Commit to Regular Plan Reviews

Your estate plan is a living document, not a file you sign once and forget. As your life and real estate portfolio evolve, your plan must keep pace. We recommend reviewing your trust every three to five years, or after any significant life event. For investors, this includes buying or selling a property, a change in family dynamics like a marriage or new grandchild, or even shifts in California law. An outdated plan can create serious problems, leaving unclear instructions for a property you sold years ago or failing to account for new assets. Regular reviews ensure your plan accurately reflects your current wishes and gives your successor trustee the clear authority needed to manage your portfolio. This simple step is crucial for protecting your legacy and preventing future family disputes. Keeping your estate plan current is a small investment to safeguard a lifetime of work.

Key Takeaways

- Use a revocable living trust as your foundation: A trust is essential for any real estate investor because it allows your properties to bypass the slow and expensive California probate process. It also provides critical protection if you become incapacitated, letting your chosen successor trustee manage your portfolio without court intervention.

- Combine an LLC with your trust for complete protection: An LLC shields your personal assets from lawsuits related to your rental properties, providing liability protection. By making your trust the owner of the LLC, you get both liability protection during your life and probate avoidance after your death.

- Plan for California’s specific tax rules: Your strategy must account for Proposition 19, which will cause your rental properties to be reassessed at current market value upon inheritance, increasing property taxes for your heirs. Holding appreciated properties in your trust until death also allows your heirs to receive a stepped-up basis, which can save them a fortune in capital gains taxes.